Ask a new DSE investor what stock to buy and they will have an answer instantly. Ask them how much to invest in that stock and you will get a blank stare. Yet position sizing — deciding how much capital to allocate to each investment — is arguably more important than stock selection itself.

A great stock pick with terrible position sizing can still lose you significant money. A mediocre stock pick with proper position sizing limits the damage. This post will give you a practical framework for managing risk across your DSE portfolio.

The Core Principle: Survive First, Profit Second

The single most important rule of investing is: do not lose so much that you cannot recover. A 50% loss requires a 100% gain just to break even. A 75% loss requires a 300% gain. The math is brutal and asymmetric.

Your position sizing strategy should be designed around this principle. Before asking “how much can I make?” always ask “how much can I lose, and can I handle it?”

Rule 1: The Maximum Position Size

No single stock should represent more than 10-15% of your total portfolio. This is not a suggestion — it is a survival rule.

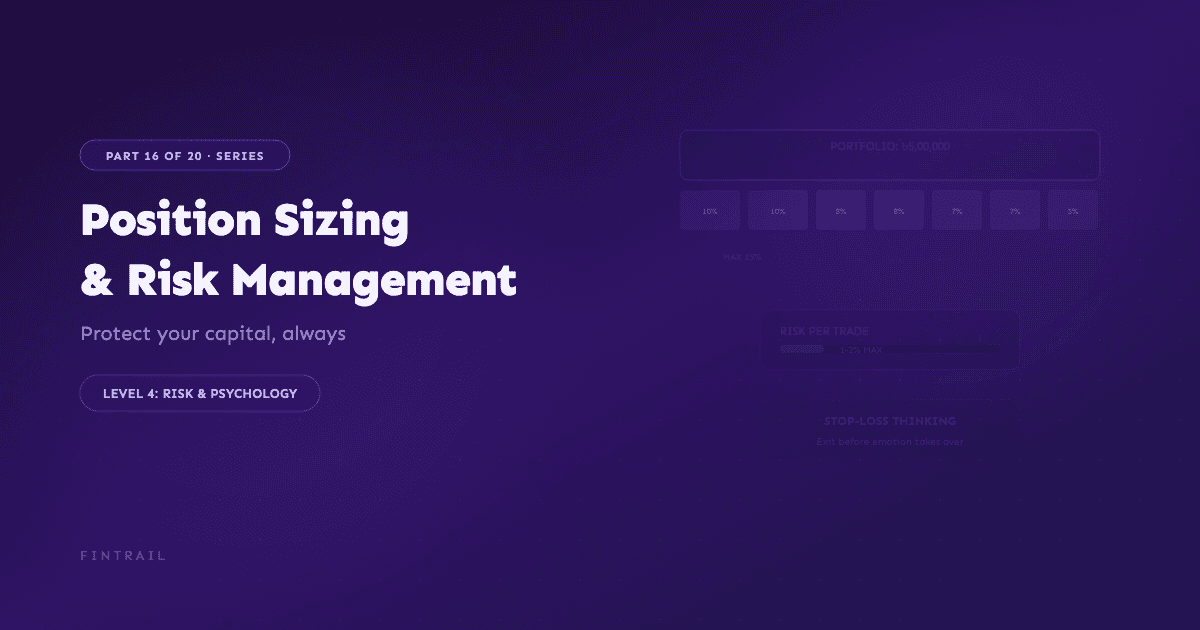

Example with a ৳5,00,000 portfolio:

If you limit each position to 10%, the maximum you invest in any single stock is ৳50,000. If that stock drops 50% — a severe but not unprecedented decline on the DSE — you lose ৳25,000, which is 5% of your total portfolio. That hurts but it is recoverable.

Now imagine you put 40% of your portfolio (৳2,00,000) into that same stock. A 50% decline costs you ৳1,00,000 — a 20% hit to your total portfolio from a single position. That is much harder to recover from, both financially and psychologically.

| Position Size | Stock Drops 30% | Stock Drops 50% | Portfolio Impact (30%) | Portfolio Impact (50%) |

|---|---|---|---|---|

| 5% (৳25,000) | -৳7,500 | -৳12,500 | -1.5% | -2.5% |

| 10% (৳50,000) | -৳15,000 | -৳25,000 | -3.0% | -5.0% |

| 15% (৳75,000) | -৳22,500 | -৳37,500 | -4.5% | -7.5% |

| 30% (৳1,50,000) | -৳45,000 | -৳75,000 | -9.0% | -15.0% |

The table makes the case clearly: larger positions create disproportionate risk.

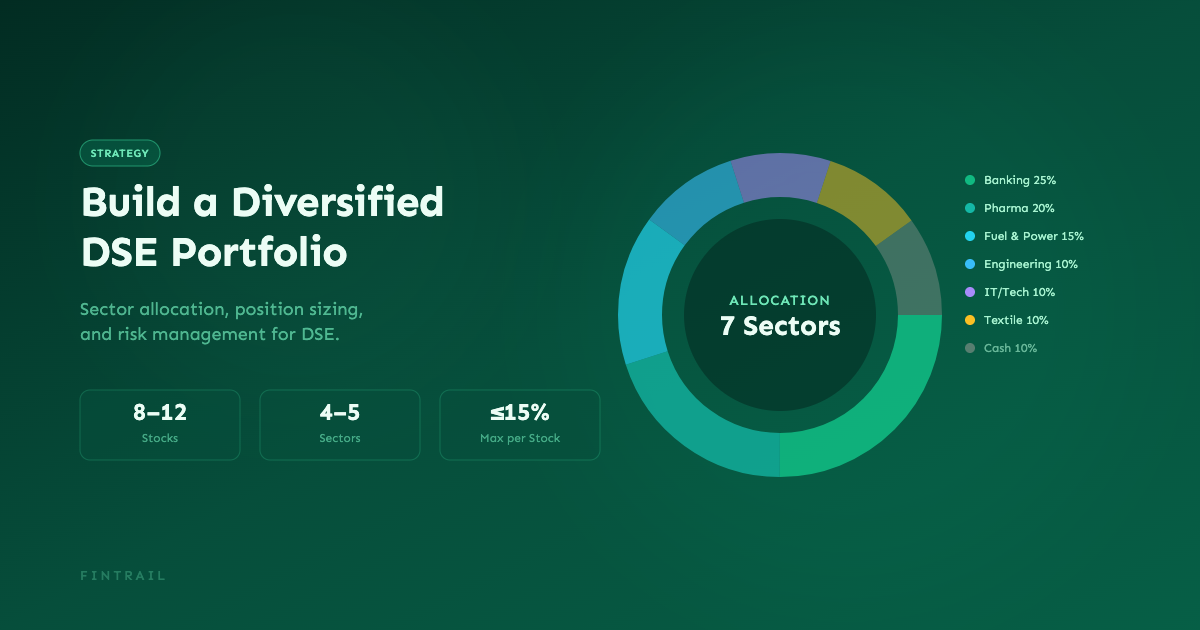

Rule 2: Sector Concentration Limits

Even if you limit individual positions to 10%, you can still be overexposed if multiple positions are in the same sector. Banking stocks on the DSE tend to move together. If you own five bank stocks at 10% each, you effectively have a 50% bet on the banking sector.

Recommended sector limits:

- Maximum 25-30% in any single sector

- Spread across at least 4-5 different sectors

- Consider sector correlation — banking and insurance often move together, so treat them as related exposure

Example: In your ৳5,00,000 portfolio, a 25% sector cap means no more than ৳1,25,000 in banking stocks total. That might be two bank stocks at ৳50,000 and ৳75,000 — not five bank stocks because “they all look cheap.”

Rule 3: Mental Stop-Losses

The DSE does not support automated stop-loss orders through most broker platforms. This means you need mental stop-losses — predetermined price levels at which you will sell a losing position.

A mental stop-loss is not a precise trigger. It is a framework for thinking about losses:

Percentage-based stop: “I will seriously consider selling any stock that drops 15-20% below my purchase price, unless the fundamental thesis remains intact.”

Fundamental stop: “I will sell if the company reports two consecutive quarters of declining earnings, regardless of stock price.”

Time stop: “If this stock has not performed as expected within 12 months, I will reassess whether my thesis was wrong.”

The key word is “seriously consider” rather than “automatically sell.” Sometimes a good stock drops 15% because the overall market is weak, not because anything is wrong with the company. The mental stop-loss forces you to actively re-evaluate rather than passively hope.

Example: You buy a pharmaceutical stock at ৳350, investing ৳70,000 (200 shares). Your mental stop-loss is at ৳297 — a 15% decline. The stock drops to ৳290 and you review the fundamentals. If the latest quarterly earnings are still growing, you might hold. If earnings have declined and the company lost a major export contract, you sell at ৳290 and accept the ৳12,000 loss rather than riding it down further.

Rule 4: The Portfolio Risk Cap

Beyond individual positions and sectors, set an overall limit on how much of your total capital you are willing to lose before stepping back entirely.

A reasonable portfolio risk cap might be 20-25%. If your total portfolio drops 20% from its invested value, stop buying, reassess all positions, and consider whether market conditions have fundamentally changed.

Example: You invested ৳8,00,000 across 10 stocks. Your portfolio risk cap is 20%, meaning at ৳6,40,000 you stop and reassess. This prevents the behavior of “averaging down” into a declining market until you have no capital left.

Rule 5: Never Invest Money You Cannot Afford to Lose

This is the most important rule and the one most frequently violated in Bangladesh. Your stock market capital should only come from money that meets all of these criteria:

- It is not needed for rent, food, utilities, or other essentials for the next 2-3 years

- It is not borrowed — not from banks, not from relatives, not from moneylenders

- It is not earmarked for children’s education, medical emergencies, or other non-negotiable expenses

- Losing 50% of it would be painful but not life-altering

If you earn ৳60,000 per month and your essential expenses are ৳45,000, your investable surplus is ৳15,000 per month at most — and you should probably keep some of that as an emergency cash reserve before investing any of it.

The 2010 crash destroyed families not because people invested in stocks, but because they invested money they could not afford to lose — savings meant for dowries, education, and medical care.

Putting It All Together: A Sample Risk Framework

Here is a complete risk management framework for a ৳6,00,000 DSE portfolio:

Position rules:

- Maximum 10% per stock (৳60,000)

- Target 8-12 stocks for diversification

- Maximum 25% per sector (৳1,50,000)

Exit rules:

- Mental stop-loss at 15% decline, with mandatory fundamental review

- Sell if investment thesis is broken regardless of price

- Take partial profits when a stock rises 50%+ (sell half, let the rest run)

Portfolio rules:

- 20% portfolio risk cap — full reassessment if portfolio drops below ৳4,80,000

- Maintain 5-10% cash reserve (৳30,000-60,000) for opportunities

- Monthly review of all positions and sector allocation

Capital rules:

- Only invest from surplus income after all expenses and emergency fund

- Never borrow to invest

- New monthly investment capped at ৳15,000-20,000 depending on income

The Role of Tracking

Risk management only works if you actually know what your current risk exposure looks like. This means tracking:

- Your cost basis for every position

- Your current allocation percentages by stock and sector

- Your unrealized P&L on every position

- Your distance from stop-loss levels

Doing this manually is tedious and error-prone. FinTrail tracks all of this automatically — showing your portfolio allocation, per-stock P&L, and sector concentration in real time. When you can see at a glance that your banking exposure has crept up to 32%, you know it is time to rebalance before adding another bank stock.

Risk Management Is Not Exciting — That Is the Point

Nothing in this post will make you rich quickly. Position sizing and risk management are not about maximizing returns. They are about ensuring that when you are wrong — and you will be wrong — the damage is contained and recoverable.

The investors who survive and thrive on the DSE over decades are not the ones who picked the most winners. They are the ones who managed their losers. A portfolio that avoids catastrophic losses and compounds steadily at even 12-15% per year will outperform a portfolio of wild swings and devastating drawdowns.

Play the long game. Size your positions carefully. Protect your capital. Let time and compounding do the work.

Think About This

- What is your current largest single position as a percentage of your total portfolio? Is it within the 10-15% guideline?

- If three of your stocks dropped 30% simultaneously, would your portfolio survive? Calculate the actual impact.

- Is any of your invested capital money you genuinely cannot afford to lose? Be honest with yourself.